The Affordable Care Act at the Brink

- Paul Francis and Adrienne Anderson

- Dec 9, 2025

- 27 min read

PDF available:

Introduction

As of this writing, the fate of enhanced premium tax credits (PTCs) for health insurance plans offered under the Affordable Care Act (ACA) is far from clear. The Senate is expected to vote on the “clean,” hereafter “straight, extension of PTCs that Republicans promised in connection with ending the government shutdown, along with an alternative Republican proposal. Neither side is expected to gain the 60 votes necessary for passage. January 30, 2026, the date the current Continuing Resolution for funding the federal government expires, is now being described as the “real” deadline for action.

If you have been trying to follow this ongoing debate, you are to be forgiven if you have little to no idea what people are talking about. Alternatives to a straight extension of the enhanced PTCs remain conceptual until specific legislation is introduced, so it is not even entirely clear what the alternatives are. Nevertheless, this issue is not going away. The purpose of this Issue Brief is to clarify the terms of debate about the enhanced PTCs and the future of the ACA. We will supplement this paper as the enhanced PTC debate evolves in Congress.

Some of the alternative proposals to a straight extension of enhanced PTCs are technical, such as imposing new income limits and minimum member contributions. But it is expected that, at least in the Senate, an alternative proposal will be made that goes to the basic construct of the ACA. The fact is that there is much that needs fixing to achieve the original vision of the ACA. Simply put, the data suggests that unless the ACA subsidies are so high that they require a minimal member contribution to premiums, ACA plans represent a poor value proposition that healthier people are unwilling to pay for – leaving large parts of the working class and middle class, for whom the ACA was intended, uninsured.

As discussed in this paper, the most intriguing alternative proposal to a straight extension of the enhanced PTCs, which is being advanced by Sen. Bill Cassidy of Louisiana, would shift a portion of federal subsidies from upfront premium tax credits to health savings accounts for individuals in Bronze plans. Any change in the basic construct of the ACA will create winners and losers. The Cassidy proposal would benefit healthier people and those with higher incomes at the expense of high utilizers and those with lower incomes who need health insurance the most.

The alternative proposals address an inconvenient truth about the ACA – which is that the level of participation is low, except in cases where member premium contributions are minimal. The source of the reluctance is both the member premium contribution at relatively moderate income levels and the high level of cost-sharing. For example, nationally, at 250% of the federal poverty level for a Silver plan, the member premium contribution is $2,115, and estimated cost-sharing is $1,610. In New York, for that same income level and for a Silver plan, the member premium contribution is also $2,115, and estimated cost-sharing is $2,560. These member premium contributions reflect a 2% share of household income at enhanced PTC levels, which will double to 4% of income if the enhanced PTCs are allowed to expire.

***

To begin with the basics, the enhanced PTCs, which were implemented in connection with the Inflation Reduction Act for a five-year period in 2021, significantly reduce the sliding-scale percentage of household income that individuals must pay to purchase a comprehensive healthcare insurance plan through an ACA marketplace with the benefit of “premium tax credits” – i.e., federal subsidies that pay for the remaining cost of the plan after the member contribution. As shown in the table below, if the enhanced PTCs implemented are not renewed and therefore allowed to lapse at the end of 2025, the increase in the portion of premiums that individuals (a.k.a. “members”) will be required to pay toward an ACA plan will increase dramatically, likely causing many individuals who are currently insured to choose to go without insurance.

This table below (also in Step Two’s previous Issue Brief: “How Many New Yorkers Will Become Uninsured Due to the One Big Beautiful Bill Act?”) displays expected member contributions based on household income as a percentage of the federal poverty level (FPL), for individual coverage with a household size of two, to purchase the second lowest cost Silver plan (SLCSP) in downstate New York. It shows the benefit of enhanced PTCs compared to the original PTC rates to which plans will revert unless Congress takes action to extend the enhanced benefits:

As shown in the figure below, the significant reduction in member contributions that resulted from the enhanced PTCs in 2021 led to a dramatic increase in the number of individuals enrolled in an ACA plan.

The central tension of the ACA has always been to balance the competing goals of (i) making comprehensive health insurance affordable for those with pre-existing conditions or demographic characteristics such as older age that likely make them high utilizers of healthcare services, while (ii) making ACA plans sufficiently affordable that large numbers of healthy individuals will choose to participate by purchasing a health insurance plan.

This latter goal of inducing large numbers of healthy individuals to purchase health insurance reflects the policy desire to reduce the number of uninsured individuals so they can have better access to healthcare, but more significantly, it is essential to the fiscal architecture of the ACA, which requires substantial participation by relatively healthy individuals to cross-subsidize those with higher expected costs.

Last year, in our commentary titled, “The Affordability of Healthcare in New York,” we observed that any discussion about affordability needed to begin by answering the question, “affordable for whom?” That paper addressed the question in the context of affordability for individuals, taxpayers, and employers. The debate about the extension of enhanced PTCs is about answering the question, “affordable for whom?” among individuals, specifically those who will become uninsured without purchasing commercial insurance.

Healthcare coverage occupies a complicated position within the “crisis of affordability” that is widely seen as the most significant challenge facing the country. If your household income is low enough to qualify for Medicaid or similar comprehensive coverage, such as New York’s Essential Plan, or you are fortunate enough to participate in an employer-sponsored plan with heavily subsidized premiums and a relatively low deductible, copayment, and coinsurance structure, healthcare is not directly contributing to your rising cost of living.

On the other hand, if you need to purchase an individual insurance policy, or if you have a high-deductible employer-sponsored plan, as approximately 42% of Americans with employer-sponsored coverage now have,[iv] the cost of paying premiums to obtain health insurance coverage itself, and fulfilling deductible, copayment, and coinsurance obligations to pay for services, may be a significant amount of your household budget.

Even with enhanced PTCs, the value proposition of purchasing an ACA health plan is weak for relatively healthy people. The data suggest that health insurance is not considered “affordable” by large numbers of eligible individuals when they are required to contribute more than a nominal percentage of their household income, in part because of the significant amount of cost-sharing (i.e., out-of-pocket spending, including the deductible and copayments or coinsurance) that is required of those with even working-class incomes.

The proposed Republican alternatives to a straight extension of the enhanced PTCs are basically designed to make ACA plans more attractive to relatively healthy individuals by reducing cost-sharing, even at the expense of higher member contributions toward premiums. Perhaps the most prominent alternative to a straight extension – the introduction of Health Savings Accounts (HSAs) to the ACA – would accomplish this by converting subsidies attributable to the enhanced portion of PTCs into HSAs that individuals could use to pay for cost-sharing obligations.

An interesting aspect of this “affordable for whom?” discussion is how it intersects with the larger national debate about affordability. Unlike strategies designed to reduce poverty, the current focus on affordability reflects a widely held view that daily life is becoming increasingly unaffordable for the working class and middle class. The Republican alternative that would shift some upfront premium subsidies to reduce cost-sharing at least partially shifts the ACA debate from ensuring access to healthcare for those who need it the most to one of affordability of healthcare for working-class and middle-income Americans.

Background

The Affordable Care Act, or “ACA,” was enacted in 2010 and subsidized comprehensive healthcare plans sold through government-run “Marketplaces” or exchanges that became available starting in 2014. Nationally, in 2025, 24.3 million Americans purchased a plan on an ACA government-run marketplace, reducing the share of Americans without health insurance from 15 percent in 2010 to approximately 8 percent in 2025.[v] In 2025, roughly 90% of enrollees received federal PTCs.[vi]

The ACA mandates that to be eligible for federal subsidies, plans, technically known as Qualified Health Plans (QHP) but referred to herein as “ACA plans,” must provide a defined comprehensive benefit package, limit out-of-pocket costs, and prohibit denial of coverage for pre-existing conditions. In general, QHPs also include stricter than usual caps on premium differentials for demographic factors (e.g., premiums for a 64-year-old cannot be more than three times higher than that of a 21-year-old, and premiums cannot vary by gender or health status).[vii] New York, as an aside, does not permit “age rating” under its community rating law, so there is no age-based premium differential in New York.[viii] These limits, called “community rating,” have the effect of certain members cross-subsidizing other members, making health insurance cheaper for some and more expensive for others than would be the case in a pure market system.

The economics of purchasing an ACA plan through an ACA Marketplace – which in New York is known as the New York State of Health (NYSOH) – are a function of three components: (i) the “member contribution” towards the total cost of the plan, (ii) the federal subsidy or “premium tax credit” that makes up the remaining cost of the plan, and (iii) the “actuarial value,” which specifies the percentage of total medical expenses the plan is expected to pay on an actuarial basis, with the remainder being made up by member cost-sharing. The Marketplace platform organizes plans into “metal” tiers that correspond to a plan’s premium costs and its cost-sharing structure, which is determined by its actuarial value.

Understanding these concepts is integral to following the current policy debate.

Member Premium Contribution

Generally speaking, the member premium contribution is based on a sliding scale of the member’s household income and household size, and whether the member is seeking coverage for just one person, or as a couple or a family with dependents under 26. However, the actual amount the member needs to pay to purchase a plan depends on the metal level (Bronze, Silver, Gold, or Platinum) of the selected plan and a formula that determines the amount of the federal subsidy or premium tax credit (PTC, which we will call the “Available PTC”).

The amount of the Available PTC is based on the difference between the total cost of the second lowest cost Silver plan in the relevant market (regardless of whether the individual purchases that plan, thus the SLCSP is sometimes referred to as the “benchmark plan”) minus the member premium contribution.

For example, in downstate New York in 2025, an individual living in a two-person household with household income equal to 250% of the federal poverty level (FPL) would be required to pay 4% of her Modified Adjusted Gross Income[ix] (hereafter, “income”) to purchase the second lowest cost Silver plan available on the New York State of Health marketplace. That would amount to $2,115. Because the total premium cost of the SLCSP in 2025 in downstate New York was $9,480, the Available PTC was $7,365.

The actual amount of the member contribution depends on the total cost of the particular plan she actually purchases. If she chose to purchase the second lowest cost Silver plan, her annual member contribution would be $2,115. However, because the total cost of the lowest cost Bronze plan in New York is $7,260, she could enroll in the Bronze plan with no member premiums, as the value of the subsidy exceeds the cost of the Bronze plan. If she chose to purchase the lowest cost Gold plan, which had a total premium cost of $12,216, her annual member contribution would be $4,851 (i.e., $12,216 minus $7,365).[x]

One of the first cracks in the foundation of the ACA was the de facto elimination of the Individual Mandate penalty as part of the first Trump tax bill in 2017. When the ACA was enacted, Congress established a penalty (which became known as the “Individual Mandate”) for individuals who chose to remain uninsured as an inducement for healthy individuals to purchase insurance. In 2017, Congress reduced the amount of this penalty to “$0,” effectively nullifying the Individual Mandate. Five states, plus Washington, D.C., adopted their own State individual mandate, but New York was not one of them, viewing the penalty as an unacceptable tax increase.[xi]

Perhaps because the amount of the Individual Mandate penalty was significantly less than the Member Contribution at most income levels, the de facto repeal of the Individual Mandate had less of an impact on enrollment than was initially expected. Nevertheless, at the margin, enrollment of fewer healthy members has the effect of increasing the total cost of a health plan and has contributed to the rising costs of ACA plans.

Federal Subsidies a.k.a. Premium Tax Credits

As shown in the graph below, federal spending on premium tax credits increased substantially as a result of the enhanced PTCs, from $57 billion in 2020 (the last year before the introduction of enhanced PTCs) to $98 billion in 2024. The Congressional Budget Office (CBO) estimates that expiration of the enhanced PTCs would reduce spending by $24.6 billion.[xii] CBO scoring from 2024 also estimated that if enhanced PTCs were permanently extended, an average of 3.8 million more people would have health insurance from 2026 to 2034 than would be the case if they expired.[xiii]

Actuarial Value and Member Cost-Sharing

The actuarial value of the plan is the percentage of the allowed costs that the insurer is expected to pay for the average member. The inverse of the actuarial value of a plan is the amount of cost-sharing in the form of deductibles, copayments, and coinsurance that an individual can actuarially be expected to pay in addition to the premium cost of the plan. “Actuarial value” is not an intuitive or familiar concept, so policymakers don’t use the term when discussing the high out-of-pocket costs that consumers face when they purchase an ACA plan. To be clear, actuarial value does not guarantee what any single person will pay, but it provides a standardized measure of the expected cost-sharing amount each metal tier requires on average.

For example, if the actuarial level of a plan is 87%, and the total cost of the plan (including the member contribution in the federal subsidy) is $9,480, then the member should expect to pay in the form of cost-sharing an amount equal to 13% times $9,480, or $1,232.

The various metal levels of QHPs offer the same comprehensive set of benefits, but differ in the level of actuarial value they offer the member. The nominal actuarial values of each metal tier are as follows:

Bronze: 60% AV

Silver: 70% AV

Gold: 80% AV

Platinum: 90% AV

The ACA allows de minimis variation around those targets (e.g., a Silver plan might be allowed to range roughly from 68–72% AV), but plans are still classified by the nearest metal target.

When adopting the ACA in 2010, Congress recognized that additional subsidies would be required to reduce the amount of cost-sharing that would be required for lower-income individuals to purchase insurance. These subsidies are known as cost-sharing reductions (CSRs), which reduce deductibles, copays, coinsurance, and out-of-pocket maximums for Silver plans for lower-income marketplace enrollees. It is important to remember that CSRs do not affect the total premium cost of the plan; they only affect the level of cost-sharing required of members at different income levels. CSRs are an even more esoteric topic than “actuarial value,” but are key to understanding the economics of the ACA.

The availability and value of CSRs in increasing the actuarial value of a plan are based entirely on the household income level of the member. Under the original federal design, the following CSR variance applied:

CSR94: income 100–150% FPL → Silver boosted to about 94% AV

CSR87: income 150–200% FPL → Silver boosted to about 87% AV

CSR73: income 200–250% FPL → Silver boosted to about 73% AV

From 2014–2017, the federal government made CSR payments to insurers to compensate them for the higher actuarial value they were obliged to provide to certain members. In 2017, the Trump administration stopped CSR reimbursements after concluding there was no specific appropriation for them.

However, insurers remained legally required under the ACA to provide CSR-enhanced Silver plans (and only to Silver plans) for eligible enrollees. To make themselves whole in the absence of funded CSR payments from the government, insurers raised Silver premiums to reflect CSR costs – a practice that became known as “Silver loading.” Because the amount of the Available PTC is tied to the cost of the second lowest cost Silver plan, this had the effect of often making Bronze plans much less expensive than Silver plans for individuals eligible for CSRs, often requiring no member contribution at all.

Beginning with plans offered in 2025, New York provided funding for CSRs that enabled an 87% actuarial value for members with household income levels between 250% and 350% of FPL, and a 73% actuarial value for members with household incomes between 350% and 400% of FPL.

New York accomplished this by providing approximately $300 million of federal funding under its Section 1332 Waiver to fund CSRs for income cohorts not eligible for CSRs under federal law. As we discussed in our paper titled “How Many New Yorkers Will Become Uninsured Due to the One Big Beautiful Bill Act?,” New York in 2024 converted its Essential Plan from its original legal authority under Section 1331 of the ACA to Section 1332 of the ACA, which was more flexible with respect to the use of federal funding for CSRs and other purposes. New York is now seeking to revert to the original Basic Health Program authority under Section 1331, and it does not appear that the State has authority to use the Basic Health Program Trust Fund to pay for state-financed CSRs. The State would either need a waiver to use 1332 funds or directly appropriate State Operating Funds to continue the State-funded CSR program.

Providing funding for these CSRs in New York likely induced at least some healthier individuals to purchase an ACA plan, improving the risk pool and thus marginally lowering the total cost of the second lowest cost Silver plan from what it otherwise would have been. Even so, as shown in the tables below, individuals in New York with household incomes up to 300% of FPL could enroll in a Bronze plan with virtually no member contribution. Even with a much higher actuarial value in a Silver plan, many New Yorkers prefer to enroll in a Bronze plan and take their chances with the higher level of cost-sharing required under a Bronze plan. The percentage of New Yorkers purchasing a Silver plan decreased from 37% in 2023 to 34% in 2025.

Total Member Cost = Premium Contribution + Cost-Sharing

Although most of the press focus in the current debate about extension of the enhanced PTCs is on the member premium contribution, the cost-sharing requirements of ACA plans are significant – especially for plans and income levels for which CSRs are not available.

The tables below illustrate the total economics of purchasing an ACA Plan and the consequences of the expiration of the enhanced PTCs. The tables below show the combined cost (“Total of Premium and Cost-Sharing”) of (i) the member contribution toward the upfront premium plus (ii) the actuarially expected member cost-sharing at different income levels and metal plan tiers – with and without enhanced PTCs.

The first set of tables below shows this based on a national average, while the second set of tables shows the information for downstate New York. The income levels of FPL are based on family size, and the tables below show the cost of an ACA plan for an individual in a two-person household. A downloadable, interactive Excel workbook of these tables with more detail can be found here.

Total Member Cost Tables

Table 1 below reflects 2025 annual total premium costs per individual of $5,964 for the second lowest cost Silver plan (SLCSP) and $4,572 for the lowest-priced Bronze plan.[xiv]

Table 1: National Total Member Cost with Enhanced Premium Tax Credits

Table 2 assumes the same FPL income levels, but reflects premium increases of 26% (the average national premium growth rate estimated for Marketplace plans for 2026) and the expiration of the enhanced PTCs. At 200% of FPL, the member contribution to premiums for purchasing the second lowest cost Silver plan without the benefit of enhanced PTCs is $2,792, versus $846 with the benefit of enhanced PTCs. It is widely thought that this will lead to consumers downgrading to a Bronze plan if they remain enrolled at all, which would make the member premium $1,038 – still more than in the current situation but roughly half the cost of purchasing the second lowest cost Silver plan.

Table 2: National Total Member Cost without Enhanced Premium Tax Credits

For Downstate New York tables, the annual premium cost per individual in 2025 was $9,480 for the second lowest cost Silver plan (SLCSP) and $7,260 for the lowest priced Bronze plan.[xv]

Table 3: Downstate New York Total Member Cost with Enhanced Premium Tax Credits

With enhanced PTCs, no member premium contribution is required to purchase a Bronze plan for individuals with household income up to 250% of FPL. Without the benefit of enhanced PTCs, as shown in Table 4, the member premium contribution for a Bronze plan would be $2,087. The impact of cost-sharing on the Total Member Cost is discussed in more detail on the next page. However, changes to the member premium contribution alone are likely to have a dramatic effect on participation levels in New York if the enhanced PTCs expire. Table 4 assumes the same FPL income levels as Table 3, but reflects premium increases of 7% (the average New York State premium growth rate estimated for Marketplace plans for 2026) and the expiration of the enhanced PTCs.

Table 4: Downstate New York Total Member Cost without Enhanced Premium Tax Credits

Consumers vote with their feet, and the evidence suggests that the combination of a non-zero member premium contribution for individuals with household incomes above 150% of FPL and low plan actuarial value (i.e., higher cost-sharing) for those with income levels above eligibility for CSRs results in a weak value proposition for ACA plans. As shown in the following table, nationally, the percentage of ACA plan enrollment among individuals with incomes at or above 250% of FPL and under 400% of FPL was only 14% in 2025, down from 20% in 2021, notwithstanding the incentive of enhanced PTCs, which cut member contributions at least in half for individuals at or below 250% of FPL.

Put another way, the cost of achieving the ACA’s goal of making health insurance comprehensive in scope and affordable for those with pre-existing conditions has become so high that it is increasingly difficult to achieve the ACA’s goal of reducing the uninsured population generally while persuading large numbers of healthy individuals to purchase insurance.

The “elasticity of demand” of obtaining health insurance coverage can be seen in New York State’s experience when it expanded eligibility for the Essential Plan to individuals with household incomes between 200% and 250% of FPL. While only about 70,000 New Yorkers in this income cohort had purchased an ACA plan with enhanced PTCs prior to this eligibility expansion, by November 2025, 468,000 New Yorkers had enrolled in the Essential Plan, which requires no member premium contribution and virtually no cost-sharing.

It is against this backdrop that the alternative proposals to a straight extension of the enhanced PTCs should be evaluated.

Alternative Proposals to a Straight Extension of Enhanced PTCs

The recent Senate Finance Committee testimony of Brian Blase, President of Paragon Health, a Republican think tank that focuses on health care reform, offers a comprehensive critique of the ACA from the perspective of many Republicans.[xvi] Blase’s critique is that the ACA’s mandates, such as comprehensive benefits and limited differentials in pricing based on pre-existing medical conditions, when combined with the ACA structure that increases federal subsidies dollar-for-dollar for increases in total premium costs, have dramatically increased the cost of healthcare while providing a windfall for insurance companies and incumbent providers. Blase doesn’t offer a specific replacement proposal for the ACA, but rather suggests redirecting federal cost-sharing subsidies directly to consumers through Health Savings Accounts (HSAs) – among other ideas focused on increasing consumer choice within and beyond the ACA marketplace.

President Trump mused publicly in recent months about redirecting all PTC subsidies into individuals’ HSAs. This idea reflects the underlying philosophy of critics of the ACA, but does not represent a serious proposal, because completely replacing premium tax credits with HSAs would fail to protect those with pre-existing conditions. Republicans have always insisted that their alternative proposals would protect individuals with pre-existing conditions. They have been frustrated since the inception of the ACA by the fact that that goal can only be achieved through the ACA’s basic construct of the pooled-risk, community-rated model, which inherently relies on cross-subsidization of more costly members by healthier members.

It is beyond the scope of this paper to address the broader critique of the ACA and any unintended consequences it has created. Instead, this paper analyzes the trade-offs involved in the most serious Republican alternative to the ACA, which involves shifting a portion of federal subsidies from reducing member premium contributions to reducing member cost-sharing, while also shifting members to plan Metal levels with lower actuarial value (e.g., Bronze plans and even Catastrophic coverage).

In the current discussion regarding extension of the enhanced PTCs, Republicans have proposed technical adjustments to the 2021 reforms that created the enhanced PTCs, such as eliminating “zero-premium” plans in which no member contribution is required, and reestablishing income limits on eligibility, which were eliminated in the 2021 changes. But the proposal that would have the most impact on the ACA involves shifting a portion of the enhanced portion of PTCs into health savings accounts that can be used to reduce cost-sharing. If adopted, this would incrementally advance a number of Republicans’ philosophical goals, including giving greater control to consumers, making healthcare more affordable for many people (while seeking to preserve access for those who need it the most, albeit at a higher price), and disintermediating insurance companies – a goal Republicans share with many on the left.

Health Savings Accounts (HSAs) are consumer-directed savings vehicles. Individuals can contribute pre-tax funds to HSAs to pay for qualified medical expenses. Employers can choose to provide a matching contribution to an HSA, and unlike a similar employer-sponsored health savings vehicle called Health Reimbursement Accounts (HRAs), HSA balances belong to the worker, accumulate year to year, and can be invested, effectively functioning as a supplemental long-term savings tool. For 2025, the IRS set contribution limits at $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution for people aged 55 and over.

It should be noted that the One Big Beautiful Bill Act (HR 1) made all Bronze and Catastrophic plans sold on ACA marketplaces HSA-eligible, effective January 1, 2026, thereby enabling individuals to pay for their cost-sharing with pre-tax dollars.[xvii] This change significantly expands the footprint of HSAs in the individual market by attaching them to the lowest-premium, highest-deductible products, just as they are found in the employer-sponsored commercial market.

The most prominent of the HSA proposals is the one being championed by Sen. Bill Cassidy of Louisiana, the Chairman of the Senate Health Committee. Sen. Cassidy has not issued a comprehensive proposal, but in concept, his plan would transfer the enhanced portion of federal healthcare subsidies related to PTCs directly to individuals in the form of HSAs, which would cover the first dollar of deductibles or other member cost-sharing expenses. He proposes to mitigate the increased member premium contributions that would result from the expiration of enhanced PTCs by incentivizing individuals to purchase a lower-cost Bronze plan instead of a Silver plan.

Sen. Cassidy’s proposal embodies three attributes that may prove to be politically popular: reducing cost-sharing for most ACA members, increasing consumer power over which healthcare services they want to spend federal subsidies on, and bypassing insurance companies with respect to this enhanced portion of federal subsidies, which increases the value of the original federal subsidies by almost 20%. These features, however, operate more by reallocating financial risk within the insured population than by reducing aggregate costs of care.

Under Sen. Cassidy’s proposal, on average, the availability of HSA funds would partially offset the higher cost-sharing percentage in a Bronze plan than in a Silver plan. However, individuals with chronic health conditions and other high utilizers of the healthcare system would wind up paying more as a result of the lower actuarial value of the Bronze plan, while healthier individuals with limited use of healthcare services would have less out-of-pocket expense because their member contribution would be similar (albeit for a Bronze plan instead of a Silver plan) while the HSA would cover a higher percentage of their cost-sharing.

The table below shows the difference in the HSA amount that would result if it were based on income cohorts, compared to providing an HSA of $1,000 across all income cohorts. If the HSA were based on income cohorts, the amount would be calculated by the difference between the member premium contribution with and without the enhanced portion of PTCs. In the case of a fixed amount, we assumed an HSA of $1,000 per member, which is based on the CBO estimate of aggregate savings of $21 billion from the elimination of enhanced PTCs divided by the estimated 85% of the 24.3 million total ACA plan members who receive premium tax credits.

Table 5: Estimated HSA Amounts Based on Income Cohorts Versus an Equal HSA Amount Across All Income Cohorts

Note: Estimates in this table are based on individual coverage for a two-person household using national average premium costs in 2025.

Irrespective of how the HSA amount is calculated, Sen. Cassidy’s HSA proposal would shift the balance of the trade-off inherent in the structure of the ACA in favor of relatively healthier people at the expense of those with pre-existing conditions or who otherwise wind up incurring significant medical expenses in a given year. It’s difficult to quantify the number of potential winners and losers under the HSA Construct, but almost by definition, the number of “winners” would outweigh the number of “losers.”

Analyzing Winners and Losers Under the HSA Construct

The tables below compare the impact on Total Member Contribution under the “HSA Construct,” which we define as the proposal by Senator Bill Cassidy to convert some of the enhanced portion of PTCs into HSAs in connection with the purchase of a Bronze plan: either the full value of the enhanced portion, which varies by income as a percentage of FPL, or a fixed amount. The lower premium cost of the Bronze plan would at least partially offset the increased member premium contribution in the absence of enhanced PTCs, while the HSA would reduce member-funded cost-sharing.

These comparisons, of necessity, reflect the average impact of policy alternatives within each income cohort and under each scenario. In reality, those individuals within each cohort who had the highest medical expenses would do worse financially than the status quo when their HSA was exhausted, while those individuals who spend at or below their HSA amount would do better financially than under the status quo.

In this presentation of the HSA Construct, we are assuming that the federally mandated, federally funded CSRs would continue to be available only for the purchase of a Silver plan. If the federally mandated CSRs were shifted to the Bronze plan (even if they remained available for the Silver plan), they would reduce cost-sharing for individuals with household income up to 150% of FPL – even further driving a shift from enrollment in Silver plans to Bronze plans.

Unless other changes are made, the deterioration of the Silver plan risk pool as people shift to lower-cost plans is likely to increase the premium costs of the “benchmark” SLCSP (and other Silver plans), resulting in greater federal subsidies on a per-member basis than exist today.

Under the HSA Construct, the “Total Member Contribution” is equal to (i) the premium contribution from the member, plus (ii) the value of the HSA, minus the actuarially expected cost-sharing from the member. Again, a downloadable, interactive Excel workbook of these tables with more detail can be found here.

The scenarios below illustrate the following scenarios, in each case compared to the status quo, i.e., the total member cost of purchasing the second lowest cost Silver Plan with enhanced PTCs.

HSA Construct with HSA amount determined by income cohort (National).

HSA Construct with HSA amount determined by fixed amount (National)

HSA Construct with HSA amount determined by income cohort with State funding of CSRs for members with income between 250% of FPL and 400% of FPL (New York)

HSA Construct with HSA amount determined by income cohort with State funding of CSRs for both Bronze and Silver plan members with income between 250% of FPL and 400% of FPL (New York)

Note: These models use average National and New York State premium values for 2025,[xviii] and for 2026, recent estimates of premium growth of 26% nationally[xix] and 7% in New York.[xx] The rate of increase in New York is lower than the expected growth nationally, in part because of the more generous State-funded CSRs.

National Scenarios

Scenario 1: HSA Construct with HSA amount determined by income cohort (National)

Scenario 2: HSA Construct with $1,000 HSA amount across all income cohorts (National)

These scenarios indicate that the HSA Construct with the HSA amount based on income cohorts would on average benefit individuals with household income at 200% of FPL and above, while those below 200% would do worse compared to the status quo. The breakeven point is higher when the HSA amount is equal across income cohorts, but less regressive for the lowest income cohorts.

New York Scenarios

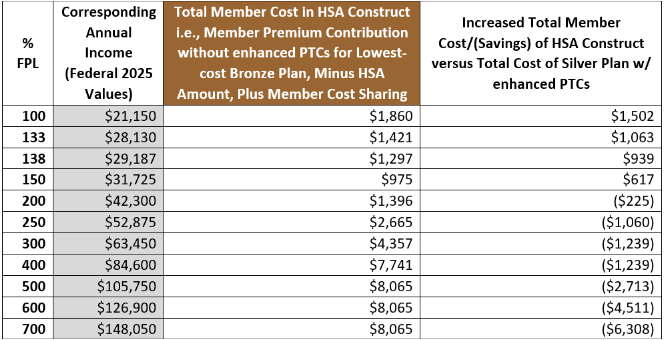

Given the much higher premium costs and federal subsidy levels in New York compared to the national average, it is likely that a fixed HSA amount would be higher than the $1,000 we calculated for the national average. However, because we do not have data on the aggregate dollar amount by which PTCs in New York would be reduced if enhanced PTCs expire, in the New York scenarios, we assume that the HSA amount is determined by the reduction in the enhanced portion of PTCs based on income cohort levels. On that basis, individuals would be better off with the HSA Construct at 200% of FPL and above (see: Scenario 3).

The amount of savings would be enhanced considerably if New York provides funding for CSRs in Bronze plans to the same extent as it does for Silver plans. In this scenario (see: Scenario 4), individuals at every income level would be better off under the HSA Construct than they are under the status quo. Although this does not personally impact individuals with incomes below 200% of FPL (who would be eligible for Medicaid or the Essential Plan), this would be highly beneficial to individuals with incomes between 200% of FPL and 250% of FPL who will be losing Essential Plan coverage, as we discussed in our previous Issue Brief, “How Many New Yorkers Will Become Uninsured Due to the One Big Beautiful Bill Act?”. These individuals would still have a Total Member Cost of $749 (compared to $0 for the Essential Plan), but that is $2,598 lower than they would need to pay to purchase the second lowest cost Silver plan with enhanced PTCs.

Scenario 3: HSA Construct with HSA amount determined by income cohort with State funding of CSRs for members with income between 250% of FPL and 400% of FPL (New York)

Scenario 4: HSA Construct with HSA amount determined by income cohort with State funding of CSRs for both Bronze and Silver plan members with income between 250% of FPL and 400% of FPL (New York)

Note: FPL tables have not yet been released for CY 2026. Assuming income levels at each % of FPL rise about 5%, Total Member Cost will also be $0 at 100% FPL.

Conclusion

The Affordable Care Act remains one of the most significant policy achievements of the past two decades, fundamentally reshaping access to health coverage. Today, however, enrollment among individuals who face more than nominal premium contributions remains relatively low—and that level of participation would fall even further if the enhanced premium tax credits are allowed to expire.

Senator Cassidy’s alternative strategy of shifting the federal subsidy associated with the enhanced portion of PTCs is intriguing. The proposal would direct more people to enroll in Bronze plans in order to reduce the member premium contribution while creating HSAs to compensate for the greater cost-sharing in Bronze plans compared to Silver plans.

For medically vulnerable populations, the effects are likely to differ in important ways. Rebalancing ACA subsidies toward lower premium plans with higher cost-sharing would tend to shift more of the burden of financial risk onto those with greater medical needs. Individuals with chronic illness, disabilities, or episodic high-cost conditions could face increased exposure once their HSA funds are depleted, particularly in states without Medicaid expansion, Basic Health Programs, such as New York’s Essential Plan, or other state-funded stopgaps, such as New York’s expanded CSRs. In those circumstances, the expiration of enhanced premium tax credits could lead individuals to forgo coverage or delay care because of higher member costs.

Even setting aside these considerations, there is broad recognition that there likely is not sufficient time to implement a complex new coverage and financing paradigm by year’s end. For that reason alone, Congress should at a minimum enact a temporary extension of the enhanced premium tax credits for at least one year to avoid the dramatic increase in member premium contributions that would make ACA plans unaffordable for many and lead them to drop insurance coverage entirely.

That said, the HSA strategy of rebalancing subsidies to create a better value proposition for ACA plans for most people is not something that should be reflexively dismissed simply because it originates from Republican policymakers. Both Republicans and Democrats should carefully examine whether such an approach could improve affordability for consumers and strengthen the risk pool by encouraging broader participation. It may well be the case that the HSA strategy would result in increased federal spending on ACA subsidies. But it would also represent a tangible contribution to addressing one of the key issues of affordability for many Americans.

The goal of the Step Two Policy Project is to make complicated issues clearer to the general public while providing evidence-based insights for policymakers. We hope that this Issue Brief advances that goal.

Endnotes:

[i] 2025 Income Levels for Medicaid, Child Health Plus and Essential Plan. New York State of Health.

[ii] Internal Revenue Service. Revenue Procedure 2024-35: Applicable Percentage Table for Premium Tax Credits. U.S. Department of the Treasury. June 2024.

[iii] Internal Revenue Service. Revenue Procedure 2025-25: Applicable Percentage Table for Premium Tax Credits for Tax Year 2026. U.S. Department of the Treasury. 2025.

[iv] Enrollment in High-deductible Health Plans Among People Younger Than Age 65 With Private Health Insurance: United States, 2019–2023. Robin A. Cohen and Elizabeth M. Briones. National Health Statistics Reports. Number 214. December 5, 2024. U.S. Centers for Disease Control.

[v] The Affordable Care Act 101. Jared Ortaliza, Matt McGough, and Cynthia Cox. KFF. October 8, 2025.

[vi] Health Insurance Tax Credits: Their Unexpected Effectiveness, and Policies to Support Them. Jeanne M. Lambrew, Aviva Aron-Dine. The Commonwealth Fund. August 13, 2025.

[viii] Marketplace Pulse: What’s at stake for enrollees over 400% FPL if enhanced premium tax credits expire? Katherine Hempstead and Matthew Valeta. Robert Wood Johnson Foundation. October 17, 2024.

[ix] Under the ACA, Modified Adjusted Gross Income (MAGI) = Adjusted Gross Income (AGI) + three specific add-backs:

1. Non-taxable Social Security benefits (including Social Security retirement and Social Security Disability Insurance payments not included in AGI)

2. Tax-exempt interest (such as municipal bond interest)

3. Foreign earned income & housing exclusions (per IRS Form 2555)

[xi] State individual mandate guide. MarshMcLennan Agency. January 2025.

[xii] Re: The Estimated Effects of Enacting Selected Health Coverage Policies on the Federal Budget and on the Number of People With Health Insurance. Congressional Budget Office. September 18, 2025. P. 13.

[xiii] Budgetary Outcomes Under Alternative Assumptions About Spending and Revenues. Congressional Budget Office. May 2024. “That overall increase in coverage consists of an increase in nongroup coverage of 7.1 million people (the net effect of an increase in subsidized nongroup coverage of 8.2 million people and a decline in unsubsidized nongroup coverage of 1.1 million people), an increase in enrollment in Medicaid and the Children’s Health Insurance Program of 500,000 people, and a decrease in employment-based coverage of 3.9 million people. The agencies estimate that the effects on coverage would be smaller in 2025 because the enhanced subsidies are already available.”

[xvi] Testimony Submitted to the Senate Finance Committee: “The Rising Cost of Health Care: Considering Meaningful Solutions for All Americans.” Brian Blase. Paragon Health Institute. November 19, 2025.

[xvii] New Rules Aim to Broaden Appeal of H.S.A.s. New York Times. November 7, 2025.

[xix] ACA Insurers Are Raising Premiums by an Estimated 26%, but Most Enrollees Could See Sharper Increases in What They Pay. October 28, 2025. KFF.

[xx] New York reveals 2026 insurance premium increases. Maya Kaufman. Politico. August 29, 2025.