How Many New Yorkers Will Become Uninsured Due to the One Big Beautiful Bill Act?

- Paul Francis and Adrienne Anderson

- Nov 12, 2025

- 38 min read

PDF available:

Introduction

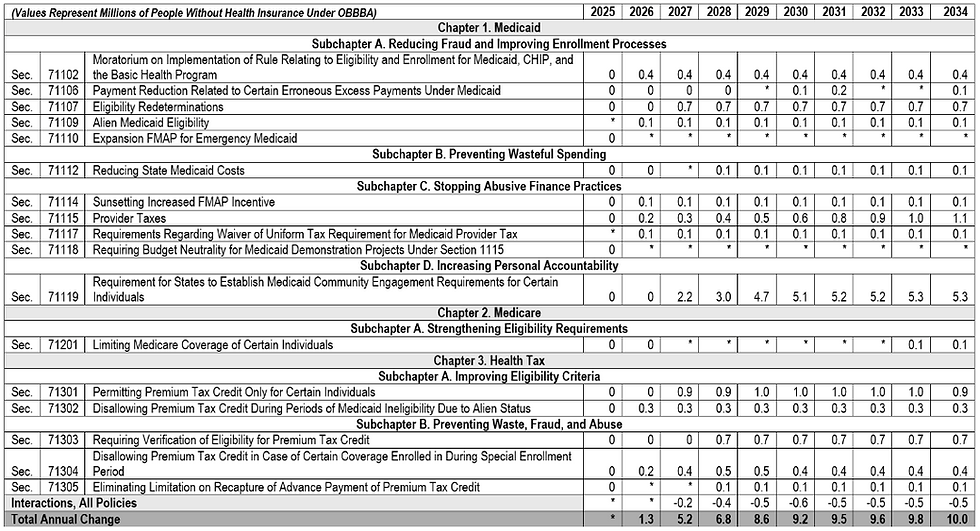

The One Big Beautiful Bill Act (OBBBA) represents one of the most consequential shifts in federal health policy in recent years. The Congressional Budget Office (CBO) estimated that over 10 years, the OBBBA would result in $990 billion in reduced Medicaid spending and cause 10 million Americans to lose health insurance coverage, with more than half of them losing coverage by 2027.[i] The Appendix of this Issue Brief shows the CBO’s anticipated coverage losses attributable to various provisions of the OBBBA.

In New York, the Hochul administration, when the OBBBA was enacted, estimated that 1.5 million New Yorkers would become uninsured as a result – an estimate that continues to be routinely cited in the press. The New York State Mid-Year Budget Update, released on November 4, 2025, softens this estimate, however, now stating: “DOH estimates as many as 750,000 to 1.5 million enrollees may be impacted” by the law.[ii]

The good news is that the high end of this estimate is likely to be greatly overstated. We suspect that even the low-end estimate of 750,000 may not accurately reflect the number of individuals who become uninsured as a result of the law, although achieving that outcome will require the State’s effective resolution of many challenging database system integration issues that result from the requirements of the OBBBA.

The bad news is that even if only several hundred thousand New Yorkers lose health coverage and become uninsured as a direct result of the policy changes in the OBBBA and the State’s related decision to rescind eligibility for the Essential Plan for New Yorkers with incomes above 200% and up to 250% (“200% -250%” for short) of the federal poverty level (FPL), it will constitute a real setback in New York’s efforts to ensure comprehensive coverage and have significant impacts on the healthcare delivery system.

We expect that loss of coverage under Medicaid due to new work requirements and redetermination rules, and loss of coverage of non-citizens under the Essential Plan, may well be less than predicted. However, based on previous coverage rates, as many as 80% of the 462,000 individuals in the 200%-250% of FPL cohort now covered by the Essential Plan (by virtue of the 1332 framework instead of the Basic Health Plan 1331 framework), may well choose to become uninsured rather than purchasing health insurance coverage using ACA marketplace premium tax credits because of the weak value proposition of those policies for healthy individuals.

Understanding the risks to continued coverage and the magnitude of possible losses of healthcare coverage requires a nuanced understanding of the provisions of the OBBBA and the statutory framework of New York’s Medicaid program and Essential Plan. It’s important to understand the tools the State has available to seek to ensure that eligible individuals do not fall through the cracks. And having an accurate sense of the likely increase in the number of uninsured New Yorkers affects both the way that New York State policymakers think about the Budget and the way healthcare providers plan for these changes. The objective of this paper is to develop a better understanding of these issues.

As of May 2025, New York State Medicaid counted 7 million members on its rolls, of whom 2.1 million (30%) are included in the “expansion population,” to which many of the new requirements of the OBBBA are targeted.[iii] Another 1.7 million New Yorkers are enrolled in the Essential Plan, which also offers comprehensive healthcare coverage at virtually no cost to its members. The risks of these individuals becoming uninsured as a result of the OBBBA are discussed in more detail below.

OBBBA/HR1 Provisions Affecting Eligibility for Medicaid and ACA Tax Credits

The “One Big Beautiful Bill Act” is also known as “HR 1.” Both political parties are guilty of creating Orwellian titles for bills (see e.g., the “Inflation Reduction Act”). Since that is not a practice we like to encourage, we will hereafter refer to the OBBBA as “HR 1”. HR 1 contains a number of provisions that will cause people who are currently eligible for Medicaid or New York’s Essential Plan to lose healthcare coverage that will not otherwise be replaced. The most significant of these provisions include:

effective January 1, 2027, imposing “work requirements” (technically called “community engagement” requirements) for eligibility for Medicaid, but only for “expansion population adults,” i.e., those enrollees with incomes up to 138% of the federal poverty level (FPL) who became eligible for coverage under the Affordable Care Act’s (ACA) Medicaid expansion;[iv]

effective January 1, 2027, requiring more frequent redetermination of eligibility for Medicaid, but only for expansion population adults; and

effective January 1, 2026, eliminating premium tax credit eligibility on New York’s Essential Plan for most lawfully present non-citizens without Green Cards who have incomes below 100% FPL but are ineligible for Medicaid due to immigration status; effective October 1, 2026, eliminating federally-funded Medicaid eligibility for most lawfully present non-citizens without Green Cards who have incomes between 100%-138% of FPL; and effective January 1, 2027, eliminating premium tax credit eligibility on NY’s health insurance marketplace – NYSOH – for most other lawfully present non-citizens without Green Cards; and

the indirect impact of the HR 1 provisions deeming most non-citizens ineligible for federally-funded healthcare coverage is that it changes the economics of the Essential Plan in a way that led the State to eliminate Essential Plan eligibility for citizens and non-citizens alike with incomes between 201%-250% of FPL. This will lead many, if not most, of the 462,000 individuals in this income cohort who are now enrolled in the Essential Plan to become uninsured, even though most of them are eligible for premium tax credits under the ACA, because the value proposition of Marketplace coverage is so much worse than the Essential Plan, with materially higher premiums, co-pays and deductibles for the same scope of coverage.

Although unrelated to HR 1, another factor that could cause an increase in the number of uninsured individuals is the sunset of the enhanced premium tax credits, which were enacted on a temporary basis in 2021, extended in 2022, and continue only through 2025.[v] The federal government has been shut down since October 1, 2025, as Democrats and Republicans battle over whether these enhanced premium tax credit subsidies will be extended.

How ACA Marketplace Premium Tax Credits Work

The way that ACA marketplace premium tax credits (PTCs) work is not well understood, which contributes to confusion about this issue. Under the ACA, individuals pay a percentage of their income toward the purchase of an individual health insurance policy on the ACA marketplace. The required member contribution is determined on a sliding scale based on household income as a percentage of FPL and on the number of individuals in the household who need coverage. The amount of the member contribution is based on the household income, even if only one person in the household is purchasing coverage.

The federal government pays directly to insurance carriers an amount equal to the difference between the cost of the second-lowest “Silver” plan policy on the ACA marketplace (i.e., the benchmark plan) and the member contribution toward the cost of the policy.[vi] The income cap for eligibility for PTCs was lifted in 2021 from the original limit of 400% of FPL. If the benchmark plan’s premium is more than 8.5% of household income, the applicant qualifies for PTCs.[vii]

For example, an individual whose two-person household income is equal to 250% of FPL ($52,875) would pay 4% of their income toward premiums. Because the cost of the second-lowest Silver Plan in downstate New York is approximately $9,650,[viii] if the individual was purchasing a policy from the insurance plan offering the second-lowest Silver plan price, the individual would pay $2,115 annually (which would be $4,463 if enhanced PTCs are not continued), and the federal government would pay the balance of approximately $7,485 (or $5,187 without enhanced PTCs) toward the cost of the policy. The amount of that subsidy is the same irrespective of the plan “metal” level the individual chooses.

Because the federal government is obligated to pay at least $7,485 (assuming enhanced PTCs) towards the purchase of a policy in this situation, and the annual premium cost of the lowest-priced Bronze plan in downstate New York is only $7,428,[ix] the federal government would pay the entire cost of the policy for an individual who had a household income of 250% of FPL. Because no member contribution would be required, this has led to criticism from opponents of the ACA that these individuals have no “skin in the game.”

The table below shows the differences in the individual’s cost of insurance coverage purchased through the NYSOH with and without enhanced PTCs. The required contribution ranges are based on the assumption that the individual seeking coverage is residing in a two-person household:

For an individual in a household with income of 200% of FPL, the out-of-pocket premium cost will more than triple if the enhanced PTCs are not renewed. So you hear Democrats (and Marjorie Taylor Greene) talking about the cost of insurance doubling for their constituents, which you can see in the table above. By the same token, the only increase in the total cost of the plan itself is effectively in the deterioration of the risk pool as a result of fewer healthy people buying insurance – the actuarial effect of which nationally is about 3%. So Republicans say that the impact of the expiration of enhanced PTCs on the cost of an insurance policy is only 3%. Both statements are true.

Approximately 240,000 New Yorkers were enrolled in NYSOH Marketplace insurance plans (qualified health plans, or QHPs) in February 2025, with approximately 140,000 receiving enhanced PTCs.[xiii] Although in other states enrollment in Marketplace plans increased dramatically with the benefit of enhanced premium subsidies, the lack of more recent public information makes that more difficult to evaluate in New York. We know that only about 5%, or approximately 7,000, more New Yorkers were enrolled in Marketplace policies in 2021,[xiv] shortly after the reduction in the member contribution due to the enhanced premium tax credits, than was the case in February 2025 – but this data might be distorted by the effects of the Covid pandemic.[xv]

What is lost in the discussion about enhanced premium tax credits is that their low “actuarial value” makes these policies unattractive for most healthy people. The actuarial value of a Silver plan is approximately 70%, which means that the plan is designed to require out-of-pocket expenses in the form of deductibles, coinsurance, and copayments of approximately 30% of the annual cost of the policy. Given that the total cost of the second-lowest Silver plan policy in downstate New York in 2024 was approximately $9,650 for an individual,[xvi] this means that the policyholder actuarially would be expected to pay approximately $2,895 annually for their coverage, across a deductible, co-payments, and coinsurance. This is in addition to the member premium contribution, which, as shown in the table above, for an individual in a household of 2 at an income of 250% FPL, is $2,115 — not a trivial amount of after-tax income. As a result, many New Yorkers who are healthy may rationally choose to remain uninsured even if enhanced PTCs become available again.

It is far from clear whether Congress will eventually approve some modified version of enhanced PTCs, although we continue to believe that the political pressure is such that it will preserve much of the enhanced benefits. Enrollment will certainly decline if enhanced PTCs lapse entirely. The resulting impairment of the risk pool would lead to even higher premium rates, increasing fears of a “doom loop” in enrollment.

We explain later in this Issue Brief how premium tax credits interact with state programs such as a Basic Health Plan (the original basis of New York’s Essential Plan), which have received authority from the federal government to pool PTCs attributed to a certain population and use those funds to provide coverage for that population through a non-Medicaid plan (in the case of a Basic Health Plan under a section 1331 Waiver) or through State-only Medicaid (in the case of a section 1332 Waiver).

Work Requirements

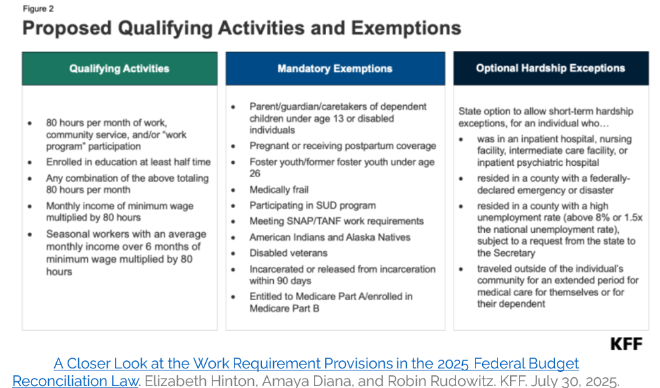

The CBO estimated that about half of the 10 million individuals losing health insurance coverage as a result of HR 1 would be a consequence of what are technically called “community engagement” requirements under the law, but which are colloquially known as “work requirements.” As is the case with most of the provisions of HR 1, work requirements do not take effect until after the 2026 midterm elections. Effective January 1, 2027, HR 1 introduces a work requirement for able-bodied adults ages 19 to 64 who are included within the Medicaid “expansion population” (i.e., all adult enrollees with incomes up to 133% of FPL, plus a 5% income disregard, for an effective ceiling of 138% FPL). There are, however, many “qualifying activities” and exemptions from the requirement, as we describe below.

Those to whom work requirements do apply must complete at least 80 hours per month of work, community service, participation in a job training program, or enrollment in an educational program at least half-time. Individuals not meeting or exempt from the work requirement by virtue of the number of hours worked or other qualifying activity may alternatively demonstrate compliance by showing monthly income equal to at least 80 hours at the federal minimum wage, currently $580 (using the federal minimum wage of $7.25), with seasonal workers allowed to average income over a six-month period. Because the State minimum wage in New York will be approximately $17.50 per hour by January 1, 2027, an individual would only need to work approximately 33 hours to earn the equivalent of 80 hours at the federal minimum wage and to qualify for this exemption.

The table below from the Kaiser Family Foundation summarizes the qualifying activities and exemptions from the “work/community engagement” requirement:

States may not broaden or add new exemption categories, nor suspend the rules during a recession or public health emergency. To enroll in Medicaid, individuals must meet the requirements for at least one month before application, though states may require up to three consecutive months of verified activity. New York is not expected to opt into any additional restrictions afforded through HR 1, including this one.

The interplay between the provision requiring eligibility for one month before application and the new limitations under HR 1 on retroactive eligibility[xvii] may result in the State (through State-only Medicaid) or providers absorbing the cost of individuals who will meet the requirements to become eligible for Medicaid but are not enrolled prior to turning up in an emergency department or clinic. Depending on how the federal government treats these provisions, the impact on providers and/or the State could be considerable.

The federal government must issue definitive regulations under HR 1 before June 1, 2026, although it is expected that at least an interim final rule will be released by the end of this year. One of the most significant issues will be how the regulations determine the definition of “medically frail or otherwise special medical needs individuals” who are exempt from work requirements. This is the most subjective aspect of the work/community engagement requirements. The statute gives examples of other, more specific conditions that qualify for exemptions, including substance use disorder, a disabling mental disorder, a disability that significantly impairs activities of daily living, and a serious or complex medical condition. But these provisions are more focused on protections of eligibility, rather than preventing states from a liberal interpretation of eligibility for exemptions from HR 1.

The final rules are likely to track federal Medicaid regulations using the term “medically frail or… special medical needs” in the Alternative Benefit Plan context. This long-standing baseline that states use in practice is set forth in 42 CFR 440.315(f) as follows:

“The individual is medically frail or otherwise an individual with special medical needs. For these purposes, the State's definition of individuals who are medically frail or otherwise have special medical needs must at least include those individuals described in § 438.50(d)(3) of this chapter, individuals with disabling mental disorders (including children with serious emotional disturbances and adults with serious mental illness), individuals with chronic substance use disorders, individuals with serious and complex medical conditions, individuals with a physical, intellectual or developmental disability that significantly impairs their ability to perform 1 or more activities of daily living, or individuals with a disability determination based on Social Security criteria or in States that apply more restrictive criteria than the Supplemental Security Income program, the State plan criteria.”

In determining the existence of a medical frailty exemption, States rely on data-first methods plus targeted documentation. These include passive identification data methods, including social security /SSI disability records, Medicaid claims and encounter data, and Medicare entitlement (which often signals disability among those under the age of 65). These data-first methods are known as “ex parte” queries of databases, which are automated and done without contacting members directly or requiring any action on the part of the member.

If there were no database system integration issues, a very high percentage of the expansion population would be able to qualify for Medicaid eligibility through ex parte determinations. For example, satisfying SNAP work requirements is a mandatory exemption from work requirements under HR 1. The gross income eligibility requirement for SNAP is 130% of FPL,[xviii] and 78% of Medicaid enrollees also participate in SNAP.[xix] Unfortunately, the absence of an integrated eligibility system in New York State makes it difficult to match individuals across these databases.

Recognition of the complexity of integrating databases was an important factor in the conservatism of the State’s estimates of the number of individuals who could become uninsured because of the work requirements under HR 1. However, the State now has an unprecedented motivation to integrate these databases despite many years of failure that resulted from bureaucratic obstacles. We believe the State will be able to overcome these obstacles, which is one reason for our expectation that fewer people will become uninsured as a result of work requirements than the State’s estimates suggest.

Individuals are commonly allowed to self‑identify as medically frail at application, renewal, or any time, which then prompts a determination using records or lightweight documentation. The State has a variety of existing assessment standards for eligibility for various types of care, such as Health Homes, Adult Behavioral Health Home and Community-Based Services and Health Home Plus programs for individuals with serious mental illness, and long-term care, based on the need for assistance with activities of daily living. Compared to the requirement of eligibility for Long-Term Services and Supports (LTSS), which is the need for assistance with at least three activities of daily living (ADL), the Alternative Benefit Plan standard of need for assistance with one ADL is a low bar – assuming that is carried over for purposes of Medicaid eligibility under HR 1.

Because the State generally has an interest in keeping people enrolled in Medicaid, it is likely that the Department of Health’s implementation plans will align its processes to 42 CFR 440.315(f), build ex parte flags for relevant federal databases, and offer easy self‑identification with a streamlined provider‑confirmation pathway – mirroring what states (probably including New York) have done for Alternative Benefit Plan eligibility determinations. HR 1 does give individuals the ability to demonstrate that they meet the medical frailty exemption if this is not captured by the ex parte data verification process.

Once enrolled, Medicaid members must satisfy the work/community engagement requirement at least once between each six-month eligibility redetermination, but states may require proof every month. Critics of HR 1 say that “work requirements” would be more accurately described as a “work reporting” requirement, in the belief that individuals will fall through the cracks not because they don’t meet the work/community engagement requirements, but for failure of various systems to report on that fact. Georgia is the only state with an active Medicaid work requirement. As ProPublica’s Broken Pathways series found, the program has produced few employment gains while creating substantial bureaucratic barriers and considerably deterring enrollment. Pilot programs in Arkansas and New Hampshire involving work requirements for Medicaid eligibility had similar bleak experiences with large numbers of individuals either losing coverage or failing to enroll for fear that they would not meet the eligibility requirements.[xx]

However, these risks are diminished in a state like New York, which will not opt for monthly eligibility redetermination and which will make every effort to design its processes in a way that keeps members eligible. Certainly, the challenge will be greater for the gig worker or “1099” population, for which there is not currently a robust database infrastructure. It is also the case that for this population, in particular, publicity about work requirements – the nuances of which will not be well understood – will deter individuals from applying for Medicaid in the first place. But it does not make sense to extrapolate the experience of pilot programs in smaller states that do not have New York’s commitment to, and experience with, the Medicaid program.

There is no doubt that New York will face daunting administrative challenges in ensuring that everyone who qualifies for Medicaid in New York becomes enrolled and remains eligible. Nevertheless, from the standpoint of the aggregate impact on the healthcare delivery system, it seems unlikely that the totals will come close to the State’s official estimate that approximately 1.2 million Medicaid members out of the 2.1 million Medicaid members to whom these requirements apply will lose healthcare coverage as a result of work requirements or more frequent eligibility redetermination under HR 1.

Increased Frequency of Redeterminations

HR 1 raises the frequency of Medicaid eligibility redeterminations to at least semiannual verification for the expansion population. It’s unclear why Congress made this requirement (as well as work requirements) apply only to the expansion population, but that limitation significantly reduces the size of the Medicaid population facing potential loss of Medicaid coverage due to these new requirements. The reason that work requirements and semiannual verification apply only to the expansion population is most likely the fact that the federal government pays a 90% match for individuals in the expansion population compared to 50% (in New York) for other Medicaid enrollees. This suggests to us that the additional work requirements, in particular, were as much as anything a function of the need to generate projected savings to offset other costs in HR 1. This may suggest that the attitude which informs the administration of HR 1 will be more flexible than punitive.

Unlike the work requirements provisions of HR 1, which seek to limit eligibility for Medicaid, HR 1’s redetermination provisions have been rationalized as an enhanced federal effort to prevent fraud or waste, particularly when Medicaid makes payments on behalf of individuals who are covered by other forms of insurance or have otherwise become ineligible for Medicaid based on changes in circumstance. States already have measures to prevent this, so it’s not surprising that the Congressional Budget Office concluded that the majority of the projected savings from this provision stem not from cases of Medicaid ineligibility reductions but rather from the temporary or permanent loss of coverage among expansion adults who continue to qualify for Medicaid but fail to complete the renewal process.

In New York, eligibility determinations are made through two primary pathways, one for the MAGI population and another for the non-MAGI population. Eligibility for mainstream Medicaid (MAGI) is generally managed by a vendor contracted by the State to confirm eligibility for Medicaid, the Essential Plan, and eligibility for premium tax credits through the NY State of Health Marketplace based on federal and state rules. Non-MAGI eligibility, including individuals who qualify based on disability, age, or long-term care needs, is still determined through local social service districts.

Because the standard for eligibility for non-MAGI services requires eligibility for a nursing home level of care and, more recently for managed long term care, the need for assistance with at least three ADLs, it seems likely that a large majority of individuals in this category have incomes at or below 100% of FPL and thus would not fall under the ACA expansion group that will be subject to semiannual eligibility redeterminations. If they did, barring some change in circumstances that would render them ineligible for LTSS, they would, by definition, qualify for the medical frailty exemption from work requirements. Nevertheless, the State will need to ensure that local social service districts effectively administer the redetermination process to keep people from falling through the cracks.

The application for initial Medicaid eligibility requires that applicants provide proof of identity, residency, income, assets, and immigration or citizenship status. In New York State, this verification is conducted through a structured, multi-step electronic “identity-proofing” process[xxi] that begins with Experian-based personal identity questions and, if needed, verification through New York State Department of Motor Vehicles (DMV) records. If the applicant cannot be verified electronically, the NYSOH Call Center may complete identity verification using information already available through documentation from applicants’ prior interactions with state benefit systems. As an option of last resort, the applicant can submit documentation for manual identity-proofing using DOH-approved documentation forms submitted through the mobile upload app, fax, or mail.

Vulnerable populations, such as the homeless and seriously mentally ill, often don’t have ready access to these sources of proof of identity – but that is a separate issue that predates HR 1. For individuals experiencing homelessness, NYSOH may be able to utilize the most recent address on file with federal or state data sources to enable matching, even if the individual no longer resides there, before updating the address later in the application once identity proofing is complete.

Income is verified through the federal data hub established under the Affordable Care Act, which allows the NYSOH system to retrieve information from multiple federal sources: the IRS (for income from tax returns), the Social Security Administration (to confirm any Social Security income or Medicare eligibility), and the Department of Homeland Security (to verify immigration status). These federal database results are returned electronically to the State for eligibility determinations. New York State supplements this process with NYS-45 quarterly wage reporting data, reported to the Department of Labor at the individual level, which provides more current income information than annual tax data. In practice, this state wage data is used more frequently for income validation because it is timelier and often more accurate for ongoing eligibility checks.

Federal regulations provide that states should verify these eligibility factors whenever possible through ex parte data verification. When the state is unable to verify these eligibility factors through databases, the state must request additional information from the applicant (or enrollee in the case of redetermination) and preserve Medicaid coverage for at least 30 days.

Income verification is much more difficult in the case of gig workers or self-employed contractors. Current federal regulations require self-attestation plus documentation to verify earnings. “If an individual attests to self-employment income, it is compared to IRS data. If no IRS data is available, the individual is required to document their income.”[xxii] It remains to be seen how the regulations governing HR 1 will treat self-attestation.

In any event, HR 1 does not make changes to the standard for verifying income. Although more frequent redetermination may affect enrollment in cases where employment is unstable, it should not, in principle, significantly affect the number of total Medicaid enrollees. Advocates suggest that states should build documentation frameworks in order to facilitate income verification for independent contractors: e.g., requiring submission of 1099-MISC/NEC, invoices, bank statements, or self-attestation, combined with audit rights by the State.

New York is more willing to rely on self-attestation in the case of identity and residency. In the case of residency, the state seeks to use Melissa data to validate the address, but, according to the New York MAGI eligibility plan, “Ultimately, the self-attested address will be accepted even if the software is unable to verify.”[xxiii] In the case of identity, if the state cannot confirm identity via trusted data sources (such as the Social Security Administration or vital records, such as birth certificates), the state must send a renewal form and give the individual a chance (at least 30 days) to submit documentation. Coverage must continue during that window.[xxiv] However, if the State needs to rely on notification by mail, there is a process of disenrollment for individuals if there is returned mail. For identity: once verified via a trusted electronic data source, the state is not required to re-verify at every renewal.[xxv] It remains to be seen whether HR 1 changes these requirements.

Once approved, coverage currently is active for 12 months, after which recipients must complete an annual renewal process. The State requires Medicaid enrollees to notify the Medicaid program in the event that they receive insurance other than Medicaid (e.g., employer-based coverage or Medicare) or if their income changes so that they exceed income eligibility. HR 1 requires states to transition from this annual renewal schedule to a six-month recertification cycle for expansion adults beginning with renewals scheduled on or after December 31, 2026. The law also directs states to implement enhanced verification procedures, including quarterly cross-checks to identify deceased individuals and any duplicate Medicaid coverage across states.

In the aggregate, semiannual redetermination for expansion adults will reduce average Medicaid enrollment by more accurately reflecting the ongoing churn in the program. The State mitigates the impact of this routine churn due to income eligibility by auto-enrolling individuals who are not Medicaid-income eligible but are EP-eligible in an EP plan. The redetermination process for most Medicaid members is already conducted automatically by the State through an ex parte database verification process. Unlike some states, New York’s motivation will be to find ways to keep people who qualify enrolled in Medicaid, rather than finding excuses to kick them off the rolls.

That said, the administrative burden of doubling the frequency of verification for the 2.1 million individuals in the expansion population will be significant. In cases where the ex parte review does not confirm eligibility, each new renewal cycle will require additional mailings, call center capacity, data exchanges, and caseworker reviews. Evidence from the 2023–2024 Medicaid unwinding related to the Covid-era rules that prohibited disenrollment suggests that many, if not most, procedural disenrollments occurred not because of ineligibility, but because of paperwork barriers such as returned mail or unprocessed documentation.

Eliminating Eligibility of Most Non-Citizens for Federally-Funded Healthcare Coverage

The most significant change in HR 1 affecting health insurance coverage in New York is the redefinition of eligibility of certain non-citizens for federally funded healthcare coverage programs. Approximately 730,000 non-citizens in New York who are lawfully present in the United States are enrolled in the State’s Essential Plan.[xxvi] In essence, these non-citizens were permitted as “lawfully present” immigrants to receive benefits under the Essential Plan, but after HR 1, with limited exception, these individuals will not be eligible for federal benefits because of the law’s new definition of “eligible alien.”

For an in-depth description of pre-HR 1 public benefits eligibility by immigration category, this chart from the Empire Justice Center, The New York Immigration Coalition, and The Legal Aid Society is valuable. We summarized the taxonomy in a new visual below:

Only the few immigrant categories with asterisks will remain eligible for federally-funded healthcare coverage once HR 1 changes take effect.

For the purposes of this Issue Brief, we will discuss two groups: first, 506,000 individuals with incomes up to 138% of FPL (known as the “Aliessa” population”) who are income-eligible for Medicaid; and second, 224,000 lawfully present immigrants who have incomes between 138-250% FPL who are not income-eligible for Medicaid but who, prior to HR 1, were eligible for premium tax credits under the ACA. Technically, some individuals, such as non-citizens with Green Cards who are in the five-year waiting period for federal Medicaid eligibility, are included in the Aliessa population but are legal permanent residents (LPR) and are therefore considered “qualified aliens,” and are not PRUCOL. As the visual shows, a number of other groups, including refugees and asylees, are “lawfully present,” “qualified aliens,” but are not considered PRUCOL.

The group with incomes up to 138% of FPL is defined as the “Aliessa” population because of a 2001 New York State Court of Appeals decision, Aliessa v. Novello, which held that denying Medicaid benefits to otherwise eligible, lawfully residing immigrants violated the State Constitution’s equal protection provisions. This population[xxvii] – lawfully present “qualified aliens” in the five-year Medicaid waiting period, lawfully present PRUCOL immigrants, and PRUCOL-only (sometimes called “residual PRUCOL”) immigrants – was covered by State-only Medicaid prior to the ACA, which made most of them eligible to receive federal premium tax credits, which were converted into direct federal payments to the State under the Essential Plan. PRUCOL-only Aliessa immigrants have not been eligible for the Essential Plan or Marketplace coverage through qualified health plans.[xxviii]

With respect to Medicaid, effective October 1, 2026, the OBBBA will allow federal payments to states only for the care of an individual who is,

“(A)a resident of 1 of the 50 States, the District of Columbia, or a territory of the United States; and

(B)either—

(i)a citizen or national of the United States;

(ii)an alien lawfully admitted for permanent residence (emphasis added) as an immigrant as defined by sections 1101(a)(15) and 1101(a)(20) of title 8 [i.e., a Green Cardholder], excluding, among others, alien visitors, tourists, diplomats, and students who enter the United States temporarily with no intention of abandoning their residence in a foreign country;

(iii)an alien who has been granted the status of Cuban and Haitian entrant, as defined in section 501(e) of the Refugee Education Assistance Act of 1980 (Public Law 96–422); or

(iv)an individual who lawfully resides in the United States in accordance with a Compact of Free Association referred to in section 1612(b)(2)(G) of title 8.”

With respect to premium tax credits under the ACA, which also serves as the basis for federal payments to New York for enrollees in the Essential Plan, the relevant section of the federal Code currently reads,

“For purposes of this section, an individual shall be treated as lawfully present only if the individual is, and is reasonably expected to be for the entire period of enrollment for which the credit under this section is being claimed, a citizen or national of the United States or an alien lawfully present in the United States.” (Emphasis added)

Section 71301 of HR 1 introduces the term “eligible alien” to this section:

“An individual who is an alien and lawfully present shall be treated as an eligible alien (emphasis added) if such individual is, and is reasonably expected to be for the entire period of enrollment for which the credit under this section is being claimed—

(i) an alien who is lawfully admitted for permanent residence under the Immigration and Nationality Act (8 U.S.C. 1101 et seq.),

(ii) an alien who has been granted the status of Cuban and Haitian entrant, as defined in section 501(e) of the Refugee Education Assistance Act of 1980 (Public Law 96–422); or

(iii) an individual who lawfully resides in the United States in accordance with a Compact of Free Association referred to in section 402(b)(2)(G) of the Personal Responsibility and Work Opportunity Reconciliation Act of 1996 (8 U.S.C. 1612(b)(2)(G)).”

As summarized by the National Immigration Law Center, HR 1 (in Section 71302) explicitly makes the following groups, who previously qualified for ACA premium tax credits or the Essential Plan, ineligible for ACA premium tax credits:

“green card holders who are in a Medicaid waiting period [i.e., green card holders are only eligible for Medicaid if they received “qualified” immigration status five or more years earlier] and earn under 100% of the federal poverty line, people paroled into the U.S. for less than one year, people with Temporary Protected Status, people with a nonimmigrant visa, people who have applied for T or U visas, people granted employment authorization, Family Unity beneficiaries, individuals granted Deferred Enforced Departure or deferred action (excluding DACA recipients who are now excluded due to Trump administration regulations), individuals under the age of 14 with a pending application for adjustment of status, asylum, withholding of removal or for protection under the Convention Against Torture; individuals granted withholding of removal under the regulations implementing the Convention Against Torture, and individuals with a pending or approved petition for classification as a Special Immigrant Juvenile.”[xxix]

Effective January 1, 2026, OBBBA disallows premium tax credits to those ineligible for Medicaid on the basis of their “alien status.” This encompasses the Aliessa population under 100% of FPL and effectively eliminates the federal payments New York has used to cover this group via the Essential Plan.[xxx] The remainder of the Aliessa population (i.e., between 100%-138% of FPL), and the remaining lawfully present immigrants with incomes of 138%-200% of FPL will lose eligibility for premium tax credits – and New York will lose the federal payments used to cover this group via the Essential Plan – on January 1, 2027.[xxxi],[xxxii]

Although it is clear that the Essential Plan will not receive new federal payments with respect to the below 100% FPL Aliessa population after January 1, 2026, (and those with incomes equal to or greater than 100% and less than or equal to 138% of FPL after January 1, 2027) whether these individuals will lose healthcare coverage is a more complicated question. The State is almost certainly obligated to provide State-only Medicaid coverage to these approximately 506,000 individuals with incomes equal to or less than 138% of FPL who are income-eligible for Medicaid if they cannot be covered by the Essential Plan. The State has never suggested that it would cover the roughly 224,000 non-citizens enrolled in the Essential Plan with incomes greater than 138% and less than or equal to 200% of FPL. So the State included these 224,000 individuals in its estimate of 1.5 million individuals becoming uninsured as a result of HR 1.

However, the State is now pursuing a strategy to continue to provide Essential Plan coverage to all 730,000 non-citizen immigrants who meet the current standards of eligibility for the Essential Plan (excluding those with incomes above 200% of FPL) by using funds accumulated in the Basic Health Program Trust Fund (which is often referred to as the Essential Plan Trust Fund). If approved by the federal government, this strategy would enable the State to continue to provide federally funded Essential Plan benefits to this population for two to three years (based on paying all the expenses of these 730,000 members and accounting for higher reimbursement rates to providers), at which point the Trust Fund reserves would likely be exhausted. The Basic Health Program Trust Fund reserves will be supplemented by annual surpluses from the remaining Essential Plan population, although the surpluses will be lower than historical levels because of a higher average income of Essential Plan members.

Understanding this strategy requires a fairly technical discussion of the Essential Plan and changes made by the State at the end of the Biden administration. In 2015, New York launched the Essential Plan, a Basic Health Program authorized under Section 1331 of the ACA to cover adults aged 19-64 with incomes up to 200% of FPL. By 2016, the State had transferred the Aliessa population from State-only Medicaid into the Essential Plan, as well as extended Essential Plan eligibility to all New Yorkers (including both citizens and non-citizen immigrants) with incomes up to 200% FPL.[xxxiii]

The Essential Plan has since become a cornerstone of New York’s health coverage landscape, offering virtually free, comprehensive insurance coverage to approximately 1.7 million low-income and working-class adults statewide who are not eligible for Medicaid, Medicare, or employer-sponsored coverage.

Only New York, Minnesota, Oregon, and the District of Columbia have created Basic Health Plan programs, which receive federal funding equal to 95 percent of the value of the premium tax credits and cost-sharing reductions that would otherwise be provided to individuals directly through premium tax credits through the ACA Marketplace. The value of the premium tax credit is based on the cost of the second-lowest Silver plan offered on the New York State of Health (NYSOH) marketplace. In short, the federal government pays for the cost of an individual insurance policy on the NYSOH, less an amount equal to the difference between the cost of the second-lowest Silver plan policy and the member premium, which is based on a sliding scale of income. Revenue in excess of required premium payments was deposited in the Essential Plan Trust Fund up until 2024.

Because commercial insurance costs in New York are based on provider reimbursement rates that are much higher than Medicaid reimbursement rates, payments from the federal government to the Essential Plan generated revenue that greatly exceeded expenses. A few years ago, the Essential Plan increased provider reimbursement rates to roughly twice the Medicaid rate to take advantage of the surplus. Even then, however, revenues generally exceeded expenses by more than $1 billion annually. These surpluses accumulated in the Trust Fund, which had a balance of $8.8 billion as of March 31, 2025.[xxxiv]

Although only three states and the District of Columbia created Basic Health Plan programs, many other states used another federal waiver authority – section 1332 of the ACA – to achieve a similar objective of using the value of premium tax credits to support federally funded healthcare coverage to individuals with incomes above Medicaid eligibility, and, in a few cases, to provide coverage to undocumented individuals who were not eligible for Medicaid even under the pre-HR 1 requirements. Instead of creating a Basic Health Plan, the states simply gained the authority to use the federal funding they received under their section 1332 waiver to finance State-only funded Medicaid to these otherwise Medicaid-ineligible populations.

In 2024, in order to expand Essential Plan eligibility to individuals with incomes above the 200% maximum established by the Basic Health Plan statute, New York State submitted a section 1332 waiver to expand the Essential Plan’s income eligibility threshold from 200% to 250% of FPL. It is not publicly known whether the amount of revenue the State received for individuals in this income cohort exceeded their expenses, but in aggregate, the Essential Plan program was expected to continue to generate sufficient annual surpluses to finance the expanded program. The federal government approved the section 1332 waiver, and as of October 4, 2025, a total of 462,000 New Yorkers[xxxv] in this income cohort were enrolled in the Essential Plan, which retained the same name even though it began under a different type of federal waiver authority.[xxxvi] Because the amount of revenue New York received every year under the section 1332 waiver was projected to more than cover expenses on an ongoing basis, the State was willing to suspend access to reserves in the section 1331 Basic Health Program Trust Fund.

The loss of federal funding for the 730,000 non-citizen immigrants under HR 1 undermines the financial feasibility of supporting the 200%-250% of FPL cohort in the Essential Plan in two ways. First, there will be less surplus revenue from lower-income cohorts to cross-subsidize the 200%-250% of FPL cohort; and second, the State believes it can use Essential Plan Trust Fund reserves in lieu of providing State-only Medicaid to the Aliessa population, but only if it resumes access by shifting the Essential Plan back to the original section 1331 (Basic Health Plan) authority.

The State sought to address both of these problems by submitting a request on October 20, 2025, to the Centers for Medicare and Medicaid Services (CMS) to terminate its 1332 waiver and revert to the original Essential Plan, i.e., the Basic Health Plan that exists under section 1331 of the ACA.[xxxvii] Because HR 1 did not extend the new definitions of “eligible alien” to the Basic Health Plan, the State believes it can keep the 730,000 non-citizen immigrants in the Essential Plan – even though they do not meet the definition of “eligible aliens” and thus will not be supported by new federal funds – and fund their costs through the Trust Fund as long as there are available reserves.

If this strategy is successful, it will preserve Essential Plan coverage for the 506,000 individuals in the Aliessa population who otherwise would need to be covered by State-only funded Medicaid, as well as for the 224,000 lawfully present immigrants in the Essential Plan with incomes above Medicaid eligibility levels (provided their income does not exceed 200% of FPL – which is the statutory maximum under the Basic Health Plan), with respect to whom the State never contemplated providing State-only funded Medicaid coverage.

In addition to reducing the number of individuals who become uninsured as a result of HR 1, if approved by the federal government, this strategy will relieve the State of the obligation to provide State-only funded Medicaid coverage to the Aliessa population – which Budget Director Blake Washington had estimated would cost approximately $2.7 billion in FY 26. Moreover, if successful, this strategy will significantly help the hospital sector by preserving the significantly higher reimbursement rates under the Essential Plan as compared to Medicaid, as well as staving off an increase in uncompensated care for the individuals who would have lost Essential Plan coverage without gaining State-only funded Medicaid coverage.

It is not a foregone conclusion that CMS will approve the state’s request to revert to the section 1331 authority and use the Basic Health Program Trust Fund reserves to pay the costs of the lawfully present immigrant population. The FY25 Mid-Year Budget Update explains the application to CMS but continues to show the liability for State-only Medicaid coverage for the Aliessa population. A detailed legal analysis of the State’s right to revert to the section 1331 authority and use the Essential Plan Trust Fund reserves to pay for the non-citizen immigrant population is beyond the scope of this paper, but it does not appear that the federal government has a statutory basis for denying the application.

Anticipated Loss of Insurance Coverage for Individuals Earning 200-250% FPL

The loss of Essential Plan coverage for citizens and eligible aliens with incomes between 200%-250% of FPL may be collateral damage from the strategy of reverting to the section 1331 Basic Health Program framework for the Essential Plan, although it is not clear whether, in the absence of the lower-income lawfully present immigrant population, there would be sufficient revenue in the Essential Plan to continue to cover this higher-income cohort. Even if this cohort were marginally sustainable by reducing provider reimbursement rates, the ability to use the Essential Plan Trust Fund to offset State-only Medicaid payments for a few years and to preserve higher provider reimbursement rates for a few years is too valuable to pass up.

Only about 78,000 individuals in this income range chose to purchase Qualified Health Plans (QHP) through the New York State of Health marketplace prior to becoming eligible for no-premium Essential plan coverage on April 1, 2024.[xxxviii] So it is likely that most of the 462,000 enrollees in this income cohort in the Essential Plan may become uninsured (if and when the federal government gives approval to the termination of the section 1332 waiver and the reversion to the original Essential Plan).

Advocates have urged the State to use Essential Plan Trust Fund reserves to help provide coverage to this income cohort, but the State explicitly ruled this out as an option in its 1332 termination request,[xxxix] noting (in the context of public comment received about this issue):

“federal law restricts the State’s ability to use the Basic Health Program Trust Fund to provide coverage for those who do not meet the statutory definition of Basic Health Program eligible, which currently does not include those who are enrolled in [the] Essential Plan with incomes above 200% of FPL.”

Although the State’s request letter states that “New York seeks to collaborate with CMS to design and provide affordable coverage options for members who will no longer qualify for current Essential Plan waiver coverage or the BHP,”[xl] it has provided no details about how this would work and this need will have to compete with many other demands for increased spending in the State Budget.

How many New Yorkers are likely to become uninsured as a result of HR 1?

In the spring of 2025, the State began to use the estimate of 2 million New Yorkers losing their existing insurance coverage and 1.5 million New Yorkers becoming uninsured if the One Big Beautiful Bill Act passed. Presentations showed the expected impact by congressional district.[xli] Other than separating out the impact of the loss of coverage for the lawfully present immigrant population (224,000, net of the number who would be covered by State-only Medicaid), the State did not publicly offer a basis for its estimate. Although it is speculation, the State may have been influenced by a white paper produced by the Center for Budget and Policy Priorities, which suggested that, based on the experience in the few states that had Medicaid work requirement pilots, 40% of Medicaid enrollees would fail to satisfy work requirements and become uninsured. That would amount to approximately 840,000 individuals out of the 2.1 million Medicaid members in the expansion population group to which the work requirements and redetermination rules apply.

The State will eventually need to fine-tune its estimate of the number of individuals who will fall off the Medicaid rolls as a result of HR 1 in order to effectively budget. However, out-year estimates in the Executive Budget and various updates are notoriously imprecise. Because the work requirements and semiannual redetermination will not take full effect for a number of years, official estimates may remain imprecise for some time. Beyond saying that we think the estimate that 40% of the expansion population will become uninsured as a result of HR 1 seems exaggerated, we don’t have sufficient information to suggest an exact alternative number.

The number of individuals becoming uninsured as a result of HR 1 will also be less than initially believed if the State’s strategy of using Basic Health Program Trust Fund reserves to maintain insurance through the Essential Plan for the entire non-citizen population currently eligible for the Essential Plan with incomes up to 200% of FPL comes to pass. This will be a temporary reprieve – perhaps two to three years – but it will help the State navigate its upcoming Budget.

Ironically, the largest cohort of individuals who become uninsured may well be those with incomes between 200%-250% of FPL, who will no longer be supported by the Essential Plan as an indirect result of HR 1. However, this really is a reflection of fundamental weaknesses in the attractiveness of premium tax credits in New York, given the high cost of individual policies and the relatively low actuarial value, which requires significant co-pays and deductibles. The alternative of comprehensive coverage at virtually no cost through the Essential Plan is obviously compelling – but was simply not contemplated for individuals making more than 200% of FPL when the ACA was enacted.

Conclusion

We have previously made the observation that both Republicans and Democrats have an incentive to exaggerate the impact of HR 1 on Medicaid spending and insurance coverage.[xlii] As Reihan Salam, President of the Manhattan Institute, said:

“The cuts aren’t real. To lower the staggering sticker price of the reconciliation bill, Republican lawmakers had to identify hundreds of billions of dollars of CBO-approved budget cuts. But they also had to convince hospitals in their home districts that those budget cuts wouldn’t actually materialize. They did this by coming up with a series of pseudo reforms that state governments could easily game.”[xliii]

It’s understandable that elected officials who opposed HR 1 would try to paint a worst possible case scenario. The problem, however, is that the press tends to accept these assertions at face value. For example, the veteran Albany reporter, Jimmy Vielkind, wrote in mid-October:

“The massive tax and spending bill signed by President Donald Trump this summer will knock 1.5 million people off their state-backed health insurance and reduce hospital funding by an estimated $8 billion, according to Hochul’s administration. [Budget Director Blake] Washington estimates a $3 billion hit to the state’s Medicaid program in the coming fiscal year.”[xliv]

The initial estimate of the increase in the number of uninsured individuals in New York was always high, and even the bottom of the recently estimated range of 750,000-1.5 million seems conservative, assuming that the State is able to resolve database system integration issues. Moreover, the new strategy of using the Basic Health Plan Trust Fund to stave off the need to cover the Aliessa population with State-only Medicaid for at least a few years means that most of the financial hit to Medicaid will be deferred for at least a few years. The State should be applauded for identifying that strategy, which was not apparent to us when we first read HR 1.

That said, there was no need to exaggerate the potential impact of HR 1. Even if the State’s application to use the Trust Fund to pay the expenses of the entire non-citizen immigrant population for a few years is approved by the federal government, eventually, there will be a $3 billion increase in State-only Medicaid to meet the State’s constitutional obligation to extend Medicaid coverage to the Aliessa population. Even if the number of New Yorkers who become uninsured as a result of HR 1 is not 1.5 million (or even 750,000), several hundred thousand New Yorkers who currently qualify for federally-funded healthcare could become ineligible for Medicaid or otherwise become uninsured.

The percentage of Medicaid enrollees nationally who should qualify for Medicaid but who become ineligible as a result of their inability to satisfy work requirements under HR 1 – particularly with semiannual determinations – is likely to vary significantly by state. States that view the new work requirements as an opportunity for budget relief will likely see larger reductions in the Medicaid rolls than states like New York that implement the program with the goal of minimizing the number of qualified New Yorkers who fall through the cracks.

Fortunately for New York, the New York State of Health has proven to be one of the best-run administrative agencies in New York. In partnership with the Department of Health and the strong commitment of the current New York State Executive branch to provide health coverage to all New Yorkers who qualify, we can expect that New York will be among the best-performing states in creating systems that keep people from becoming uninsured because of bureaucratic problems.

Appendix: CBO's Estimate of Annual Changes in the Number of People Without Health Insurance Under Title VII, Public Law 119-21[1]

[1] Source: Internal presentation of data from the Congressional Budget Office. “These estimates are subject to considerable uncertainty. CHIP = Children’s Health Insurance Program; FMAP = federal medical assistance percentage; n.a. = not applicable; * = fewer than 50,000 people. CBO’s cost estimate for P.L. 119-21 is available online. See Congressional Budget Office, estimated budgetary effects of Public Law 119-21, to provide for reconciliation pursuant to title II of H. Con. Res. 14, relative to CBO’s January 2025 baseline (July 21, 2025), http://www.cbo.gov/publication/61570. … This table presents supplemental data for Congressional Budget Office, letter to the Honorable Brendan F. Boyle, the Honorable Hakeem Jeffries, the Honorable Jeffrey A. Merkley, and the Honorable Charles E. Schumer concerning the distributional effects of Public Law 119-21 (August 11, 2025), http://www.cbo.gov/publication/61367.”

Endnotes:

[i] New CBO Health Coverage Estimates of Budget Reconciliation Law. Edwin Park. Georgetown University McCourt School of Public Policy: Center for Children and Families. August 14, 2025.

[ii] FY2026 NYS Enacted Budget Financial Plan: Mid-Year Update. New York Governor Kathy Hochul and Budget Director Blake Washington. November 2025.

[iii] Fact Sheet: Medicaid in New York. KFF. May 2025.

[iv] The Affordable Care Act expanded Medicaid eligibility to adults with incomes up to 138% FPL (technically, 133% FPL plus a 5% disregard) and provided states with an enhanced federal match toward that population. New York adopted the expansion in 2014. (“Status of State Medicaid Expansion Decisions.” KFF. September 29, 2025.)

[v] Enhanced Premium Tax Credits for ACA Health Plans: Who They Help, and Who Gets Hurt If They’re Not Extended. Carson Richards, Sara R. Collins. The Commonwealth Fund. February 18, 2025.

[vi] Per 26 CFR 1.36B-3(f)(3).

[vii] How NY State of Health Enrollees Benefit from the American Rescue Plan and the Inflation Reduction Act. New York State of Health. October 2, 2025.

[viii] 2024 Monthly Premiums for Second Lowest Cost Silver Plans (SLCSP) by Coverage Family Type. New York State of Health.

[ix] 2024 Monthly Premium Amount of Lowest Cost Bronze Plans by Coverage Family Type. New York State of Health.

[x] 2025 Income Levels for Medicaid, Child Health Plus and Essential Plan. New York State of Health.

[xi] Internal Revenue Service. Revenue Procedure 2024-35: Applicable Percentage Table for Premium Tax Credits. U.S. Department of the Treasury. June 2024.

[xii] Internal Revenue Service. Revenue Procedure 2025-25: Applicable Percentage Table for Premium Tax Credits for Tax Year 2026. U.S. Department of the Treasury. 2025.

[xiii] Congressional District Fact Sheet. NY State of Health. 2025.

[xiv] Health Insurance Coverage Update: September 2021. NY State of Health. September 2021.

[xv] Another 36,134 are receiving Cost Sharing Reductions in 2025.

[xvi] 2024 Monthly Premiums for Second Lowest Cost Silver Plans (SLCSP) by Coverage Family Type. New York State of Health.

[xvii] The OBBBA limits retroactive Medicaid coverage from the current 90-day window to 30 days for expansion adults and 60 days for all other Medicaid members, effective January 1, 2027.

[xviii] SNAP Eligibility. U.S. Department of Agriculture. Food and Nutrition Service.

[xix] The Implications of Federal SNAP Spending Cuts on Individuals with Medicaid, Medicare and Other Health Coverage. KFF. June 26, 2025.

[xx] Medicaid Work Requirements Could Put 36 Million People at Risk of Losing Health Coverage. Gideon Lukens and Elizabeth Zhang. Center for Budget and Policy Priorities.

[xxi] Identity Proofing PowerPoint Presentation. NY State of Health. 2025.

[xxii] MAGI-based Eligibility Verification Plan: New York State. CMS. February 26, 2024.

[xxiii] Ibid.

[xxiv] CMCS Informational Bulletin: Basic Requirements for Conducting Ex Parte Renewals of Medicaid and CHIP Eligibility. Daniel Tsai. CMS. November 26, 2024.

[xxv] Medicaid Eligibility and Enrollment Rule Explainer. Tricia Brooks and Allexa Gardner. Georgetown University McCourt School of Public Policy: Center for Children and Families. April 11, 2024.

[xxvi] Understanding the Impact of the Federal Reconciliation Bill on New York. NY State of Health.

[xxvii] The Essential Plan. Amy E. Lowenstein and Andrew Leonard. Empire Justice Center and Children’s Defense Fund: New York. November 12, 2015. Slide 10.

[xxviii] Of note, DACA recipients’ status was reclassified from PRUCOL-only to “lawfully present” in 2024, thereby making them eligible for the EP and for qualified health plans. A federal rule from August 25, 2025, however, rescinded this change such that DACA status will no longer be considered “lawfully present,” and therefore is no longer eligible. See: New Federal Health Insurance Rule to Impact Coverage in New York. Troy Oeschner, Jillian Kirby Bronner, and Courtney Burke. Rockefeller Institute of Government. August 2025.

[xxix] Fact Checking Immigrants, Health Care, and the 2025 Tax and Budget Law. Ben D’Avanzo. National immigration Law Center. October 1, 2025.

[xxx] Health Provisions in the 2025 Federal Budget Reconciliation Law. KFF. August 22, 2025. See section 71302.

[xxxi] Overview: W&M and E&C Impacts on New York (as of 5/18/25). NY State of Health and New York State Department of Health.

[xxxii] The OBBBA’s Premium Tax Credit Restrictions Will Severely Harm New York, Its Hospitals, and Its Essential Plan. Greater New York Hospital Association. July 21, 2025.

[xxxiii] 16ADM-01 - Transitioning Essential Plan Consumers from WMS to NY State of Health.” Administrative Directive. New York State Department of Health. January 20, 2016. Note: pregnant women, who were eligible for State-only funded Medicaid up to 223 percent of FPL, remained ineligible for the Essential Plan because of their alternative coverage.

[xxxiv] FY2026 NYS ENACTED BUDGET Financial Plan Mid-Year Update. New York State Governor Kathy Hochul and Budget Director Blake Washington. October 2025. P. 136.

[xxxv] “EP and QHP Enrollment as of October 4, 2025.” NY State of Health. October 4, 2025.

[xxxvi] “Submission to the Centers for Medicare and Medicaid Services (CMS): New York State’s Request to Terminate the Section 1332 State Innovation Waiver and Return to the Basic Health Program.” New York State Department of Health. October 20, 2025.

[xxxvii] “Submission to the Centers for Medicare and Medicaid Services (CMS): New York State’s Request to Terminate the Section 1332 State Innovation Waiver and Return to the Basic Health Program.” New York State Department of Health. October 20, 2025.

[xxxviii] New York State Section 1332 Waiver: Annual Public Forum and Hearing. New York State Department of Health and NY State of Health. June 12 and 14, 2024. Slide 10.

[xxxix] Submission to the Centers for Medicare and Medicaid Services (CMS): New York State’s Request to Terminate the Section 1332 State Innovation Waiver and Return to the Basic Health Program. New York State Department of Health. October 20, 2025.

[xl] Submission to the Centers for Medicare and Medicaid Services (CMS). See p. 3.

[xli] Overview: W&M and E&C Impacts on New York (as of 5/18/25). New York State Department of Health and New York State of Health.

[xlii] What Happened? And What’s Next? Commentary #22. Paul Francis. Step Two Policy Project. July 24, 2025.

[xliii] Is the One Big Beautiful Bill a Masterstroke – Or a Disaster. The Free Press. July 6, 2025.

[xliv] NY faces a bleak budget just as Gov. Hochul runs for reelection. Jimmy Vielkind. Gothamist. October 13, 2025.